-

<< Back to all news<< Back to all news

August 3, 2017

Endeavour Silver Reports Financial Results For Second Quarter, 2017; Updates On Development Projects And 2017 Guidance

Vancouver, Canada – August 3, 2017 - Endeavour Silver Corp. (NYSE: EXK; TSX: EDR) released today its financial results for the second quarter ended June 30, 2017. Endeavour owns and operates three underground silver-gold mines in Mexico: the Guanaceví mine in Durango state, and the Bolañitos and El Cubo mines in Guanajuato state.

The Company's financial performance in the Second Quarter, 2017 was impacted by lower production and increased exploration and development activities compared to the Second Quarter, 2016. Production was lower in Q2, 2017 compared to Q2, 2016 due to differences in the annual mine plans. In 2016, production was higher in H1 and declined in H2 whereas in 2017, production should rise incrementally from H1 to H2 with increased access to reserves at all three mines.

Production in the Second Quarter, 2017 was higher than the First Quarter, 2017 due primarily to improved performance of the Bolañitos and El Cubo mines. Both mines are now performing in line with their operating plans for the year whereas Guanacevi continues to lag behind plan.

Highlights of Second Quarter 2017 (Compared to Second Quarter 2016)

Financial

- Net loss of $16 thousand(1) (loss of $0.00 per share) compared to net earnings of $1.7 million ($0.01 per share)

- EBITDA(2) decreased 64% to $3.7 million

- Cash flow from operations before working capital changes decreased 53% to $4.4 million

- Mine operating cash flow before taxes(1) decreased 49% to $8.8 million

- Revenue decreased 27% to $32.7 million

- Realized silver price increased 4% to $17.16 per ounce (oz) sold

- Realized gold price decreased 1% to $1,270 per oz sold

- Cash costs(2) increased 56% to $8.36 per oz silver payable (net of gold credits)

- All-in sustaining costs (AISC)(2) increased 94% to $20.46 per oz silver payable (net of gold credits)

- Working capital decreased 8% to $75.2 million from year end

Operations

- Silver production decreased 26% to 1,143,788 oz

- Gold production decreased 17% to 13,058 oz

- Silver equivalent production was 2.1 million oz (at a 70:1 silver: gold ratio)

- Silver oz sold down 34% to 988,821 oz

- Gold oz sold down 20% to 12,294 oz

- Bullion inventory at quarter-end included 226,437 oz silver and 631 oz gold

- Concentrate inventory at quarter-end included 50,644 oz silver and 890 oz gold

- Acquired the Calicanto and Veta Grande properties near the El Compas gold-silver mine project in Zacatecas, Mexico

(1) The Consolidated Interim Financial Statements and Management’s Discussion & Analysis can be viewed on the Company’s website at www.edrsilver.com, on SEDAR at www.sedar.com and EDGAR at www.sec.gov. All amounts are reported in US$

(2) Mine operating cash flow, EBITDA, cash costs and all-in sustaining costs are non-IFRS measures. Please refer to the definitions in the Company’s Management Discussion & AnalysisEndeavour CEO Bradford Cooke commented, “Our second quarter production was an improvement over the first quarter thanks to higher tonnes and/or grades from the Bolañitos and El Cubo mines. The Guanaceví mine continued to lag behind plan and another internal review was initiated in order to better understand the new issues and possible resolutions.

“At Guanaceví, power outages in the first quarter caused pump failures and some flooding underground. Slower than planned mine development due to narrower vein widths than in the resource model also contributed to lower mine output than planned, while excess dilution of the ore resulted in lower than planned grades. In July, a lightning strike caused a repeat in the electrical issues just as electrical repairs were nearing completion, resulting in another pump failure and renewed flooding in the deeper workings. Recent completion of electrical and ventilation repairs and construction of a new underground pump station should help smooth production in H2, 2017. However, given these setbacks, we have concluded that Guanacevi will not meet its planned production this year and accordingly, we are reducing our consolidated production guidance and raising our consolidated cost guidance.

“We will continue to closely monitor the operating performance at Guanacevi. Returning Guanacevi to long-term profitability relies in part on developing two new orebodies, Milache and Santa Cruz Sur. Underground ramp access is already underway towards Milache and initial production is expected in the second half of 2018. Mine development at Santa Cruz Sur is scheduled to coincide with the development of Milache.”

Mine Operations Update

In January, management guided Guanacevi 2017 production to range between 2.4 to 2.6 million silver ounces and 5,300 to 6,300 gold ounces. Due to the narrower vein widths, management now estimates production will range from 800 to 900 tonnes per day, generating 1.0 to 1.1 million silver ounces and 2,100 to 2,200 gold ounces in the second half of 2017. As a result, the revised Guanacevi 2017 full year forecast production is 2.0 to 2.1 million ounces silver and 4,400 to 4,500 ounces gold.

At Bolañitos, silver grades improved during the Second Quarter but were below plan due to grade variations in the LL-Asunción vein. The lower silver grades were offset by higher throughput than planned. Gold production exceeded plan due to higher throughput and gold grades. Management expects production on a silver equivalent basis to meet 2017 production guidance.At El Cubo, both silver and gold grades were higher than plan, and throughput was slightly below plan. During the quarter, management made changes to both mining methods and ore control processes to reduce the dilution and provide higher-grade material to the plant. Grades are expected to stabilize and throughput should regain plan through year-end with the completion of a secondary ramp to access better grades. Management expects production on a silver equivalent basis to meet 2017 production guidance.

Development Projects Update

At El Compas, work has begun on installing project infrastructure, collaring the mine access ramp and refurbishing the plant. Project engineering is being refined and optimization studies are underway on mining methods and crushing and grinding alternatives. The Company is waiting for clarification from the state government of Zacatecas regarding an exemption from the new environmental taxes. The explosives permit may take until year-end due to a substantial slowdown in the government permitting process. In the interim, mine development will proceed using a form of low impact gunpowder. Management therefore anticipates an increase in the timeline to production compared to the PEA with mine and plant commissioning now expected to commence in the first quarter, 2018.

At Terronera, work is currently focused on refinement of the project engineering and optimization studies on mining methods, crushing and grinding alternatives and power options. Similar to El Compas, permitting delays have affected the explosives, mine dumps and plant tailings permits so management does not expect to break ground on mine development until the first quarter, 2018, with mine and plant commissioning now anticipated to commence in mid-2019.

Revised 2017 Guidance

Silver production is now expected to be in the range of 4.8-5.2 million oz and gold production is expected be in the 49,100-51,200 oz range. Silver equivalent production is forecast to be 8.5-9.0 million oz using a 75:1 silver:gold ratio, as shown in the table below.

Mine Silver (M oz) Gold (K oz) Ag Eq (M oz) Tonnes/Day (tpd) Guanaceví 2.0-2.1 4.4-4.5 2.3-2.4 800-900 Bolañitos 0.9-1.0 21.5-22.5 2.5-2.7 1,000-1,100 El Cubo 1.9-2.1 23.2-24.2 3.6-3.9 1,300-1,500 Total 4.8-5.2 49.1-51.2 8.5-9.0 3,100-3,500 Using the 2017 annual guidance assumptions of $17 per oz silver price, $1,190 per oz gold price, and 20:1 Mexican peso per U.S. dollar exchange rate, cash costs, net of gold by-product credits, are now expected to be $7.00 to $8.00 per oz of silver produced in 2017. Consolidated cash costs on a co-product basis are anticipated to be $10.75 to $11.75 per oz silver and $825 to $900 per oz gold.

All-in sustaining costs of production, net of gold by-product credits in accordance with the World Gold Council standard, are estimated to be $15.25 to $16.25 per oz of silver produced in 2017. When non-cash items such as stock?based compensation are excluded, all?in sustaining costs are estimated to be in the $14.75 to $15.75 range. Direct operating costs are estimated to be in the range of $75 to $80 per tonne. Guanacevi has incurred $10.1 million to date of the annual budgeted $16.7 million in sustaining capital.

Financial Results

For the second quarter ended June 30, 2017, the Company generated revenue totaling $32.7 million (2016 - $44.5 million). During the quarter, the Company sold 988,821 silver oz and 13,058 gold oz at realized prices of $17.16 and $1,270 per oz respectively, compared to sales of 1,493,790 silver oz and 15,364 gold oz at realized prices of $16.54 and $1,289 per oz respectively in Q2, 2016.

After cost of sales of $27.2 million (2016 - $31.6 million), mine operating earnings amounted to $5.4 million (2016 –$12.9 million). Excluding depreciation and depletion of $3.3 million (2016 - $4.1 million), and share-based compensation of $0.1 million (2016- $0.2 million), mine operating cash flow before taxes was $8.8 million (2016 – $17.3 million) in Q2, 2017. Net loss was $16 thousand (2016 – net earnings of $1.7 million) after exploration expense of $3.8 million (2016 – $1.9 million) and corporate general and administrative costs of $2.4 million (2016 – $3.2 million).

Direct production costs per tonne per ounce in Q2, 2017 increased 15% compared with Q2, 2016. Reduced mining activity was offset by cost reductions and the benefits of a lower Mexican peso. Cash costs per ounce rose 56% due to the higher costs per tonne and lower silver grades. All?in sustaining costs rose as a result of management significantly increasing capital investments for the long-term benefit of Guanaceví and El Cubo operations after a two?year period of reduced capital investment to maximize cash flow and ensure the viability of its operations during times of low silver and gold prices.

Working capital dipped to $75.2 million, down 8% from December 31, 2016, more than sufficient for the Company to meet its short and medium term goals.

Conference Call

A conference call to discuss the results will be held today, Thursday, August 3rd at 10am PDT (1pm EDT). To participate in the conference call, please dial the following:

Toll-free in Canada and the US: 1-800-319-4610

Local Vancouver: 604-638-5340

Outside of Canada and the US: 1-604-638-5340No pass-code is necessary to participate in the conference call.

A replay of the conference call will be available by dialing 1-800-319-6413 in Canada and the US (toll-free) or 1-604-638-9010 outside of Canada and the US. The required pass-code is 1573 followed by the # sign. The audio replay and a written transcript will also be made available on the Company’s website at www.edrsilver.com.

About Endeavour Silver – Endeavour Silver is a mid-tier precious metals mining company that owns three high grade, underground, silver-gold mines in Mexico. Since start?up in 2004, Endeavour has grown its mining operations organically to produce 9.7 million ounces of silver and equivalents in 2016. We find, build and operate quality silver mines in a sustainable way to create real value for all stakeholders. Endeavour Silver’s shares trade on the TSX (EDR) and the NYSE (EXK).

Contact Information - For more information, please contact:

Meghan Brown, Director Investor Relations

Toll free: (877) 685-9775

Tel: (604) 640-4804

Fax: (604) 685-9744

Email: moc.revlisrde@nworbm

Website: www.edrsilver.comCautionary Note Regarding Forward-Looking Statements

This news release contains “forward-looking statements” within the meaning of the United States private securities litigation reform act of 1995 and “forward-looking information” within the meaning of applicable Canadian securities legislation. Such forward?looking statements and information herein include but are not limited to statements regarding Endeavour’s anticipated performance in 2017 including changes in mining and operations and the timing and results of various activities. The Company does not intend to, and does not assume any obligation to update such forward-looking statements or information, other than as required by applicable law.

Forward-looking statements or information involve known and unknown risks, uncertainties and other factors that may cause the actual results, level of activity, performance or achievements of Endeavour and its operations to be materially different from those expressed or implied by such statements. Such factors include, among others, changes in national and local governments, legislation, taxation, controls, regulations and political or economic developments in Canada and Mexico; financial risks due to precious metals prices, operating or technical difficulties in mineral exploration, development and mining activities; risks and hazards of mineral exploration, development and mining; the speculative nature of mineral exploration and development, risks in obtaining necessary licenses and permits, and challenges to the Company’s title to properties; as well as those factors described in the section “risk factors” contained in the Company’s most recent form 40F/Annual Information Form filed with the S.E.C. and Canadian securities regulatory authorities.

Forward-looking statements are based on assumptions management believes to be reasonable, including but not limited to: the continued operation of the Company’s mining operations, no material adverse change in the market price of commodities, mining operations will operate and the mining products will be completed in accordance with management’s expectations and achieve their stated production outcomes, and such other assumptions and factors as set out herein. Although the Company has attempted to identify important factors that could cause actual results to differ materially from those contained in forward-looking statements or information, there may be other factors that cause results to be materially different from those anticipated, described, estimated, assessed or intended. There can be no assurance that any forward-looking statements or information will prove to be accurate as actual results and future events could differ materially from those anticipated in such statements or information. Accordingly, readers should not place undue reliance on forward-looking statements or information.

ENDEAVOUR SILVER CORP.

COMPARATIVE HIGHLIGHTSThree Months Ended June 30 Q2 2017 Highlights

Six Months Ended June 30 2017 2016 % Change 2017 2016 % Change Production 1,143,788 1,551,851 (26%) Silver ounces produced 2,220,762 3,061,916 (27%) 13,058 15,649 (17%) Gold ounces produced 24,782 31,609 (22%) 1,116,799 1,511,109 (26%) Payable silver ounces produced 2,170,909 2,984,791 (27%) 12,756 15,200 (16%) Payable gold ounces produced 24,215 30,718 (21%) 2,057,848 2,725,526 (24%) Silver equivalent ounces produced(1) 3,955,502 5,274,546 (25%) 8.36 5.37 56% Cash costs per silver ounce(2) 8.09 6.49 25% 12.02 8.30 45% Total production costs per ounce(2) 11.83 9.61 23% 20.46 10.53 94% All-in sustaining costs per ounce(2) 19.38 10.82 79% 303,943 377,198 (19%) Processed tonnes 607,165 785,751 (23%) 84.01 73.01 15% Direct production costs per tonne(2) 79.90 73.66 8% 12.10 9.94 22% Silver co-product cash costs(2) 12.05 10.41 16% 896 774 16% Gold co-product cash costs(2) 878 823 7% Financial 32.7 44.5 (27%) Revenue ($ millions) 69.1 86.0 (20%) 988,821 1,493,790 (34%) Silver ounces sold 2,224,415 3,005,109 (26%) 12,294 15,364 (20%) Gold ounces sold 23,584 30,619 (23%) 17.16 16.54 4% Realized silver price per ounce 17.51 15.86 10% 1,270 1,289 (1%) Realized gold price per ounce 1,275 1,254 2% (0.0) 1.7 (101%) Net earnings (loss) ($ millions) 6.0 3.5 71% 5.5 12.9 (58%) Mine operating earnings (loss) ($ millions) 13.3 19.2 (31%) 8.8 17.3 (49%) Mine operating cash flow(8) ($ millions) 20.8 28.7 (28%) 4.4 9.4 (53%) Operating cash flow before working capital changes (2) 13.3 16.8 (21%) 3.7 10.1 (64%) Earnings before ITDA (10) 12.6 18.8 (33%) 75.2 72.1 4% Working capital ($ millions) 75.2 72.1 4% Shareholders 0.00 0.01 100% Earnings (loss) per share – basic 0.05 0.03 67% 0.03 0.08 (59%) Operating cash flow before working capital changes per share (2) 0.10 0.15 (33%) 127,318,926 113,236,504 12% Weighted average shares outstanding 127,207,961 108,941,454 17% (1) Silver equivalents are calculated using a 70:1 ratio. 2016 Silver equivalents have been restated from 75:1 to 70:1 for comparative purposes

(2) Cost metrics, EBITDA, mine operating cash flow, operating cash flow before working capital changes are non-IFRS measures. Please refer to the definitions in the Company’s Management Discussion & Analysis.ENDEAVOUR SILVER CORP.

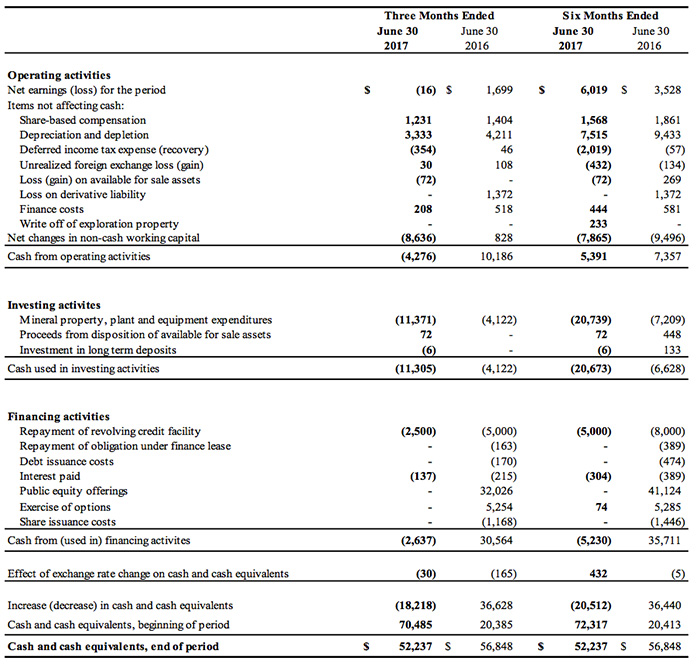

CONSOLIDATED INTERIM STATEMENTS OF CASH FLOWS

(expressed in thousands of U.S. dollars)

This statement should be read in conjunction with the condensed consolidated interim financial statements for the period ended June 30, 2017 and the related notes contained therein.

ENDEAVOUR SILVER CORP.

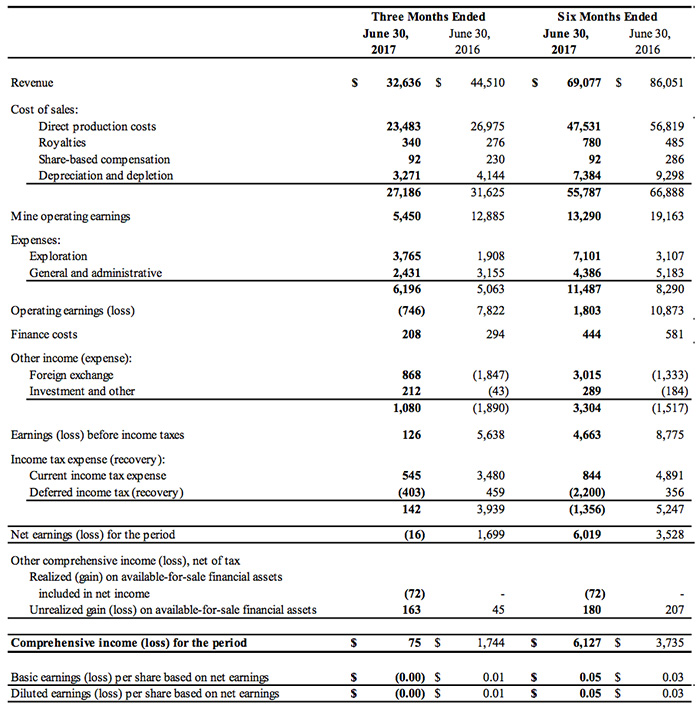

CONSOLIDATED INTERIM STATEMENTS OF COMPREHENSIVE INCOME

(expressed in thousands of US dollars, except for shares and per share amounts)

This statement should be read in conjunction with the condensed consolidated interim financial statements for the period ended June 30, 2017 and the related notes contained therein.

ENDEAVOUR SILVER CORP.

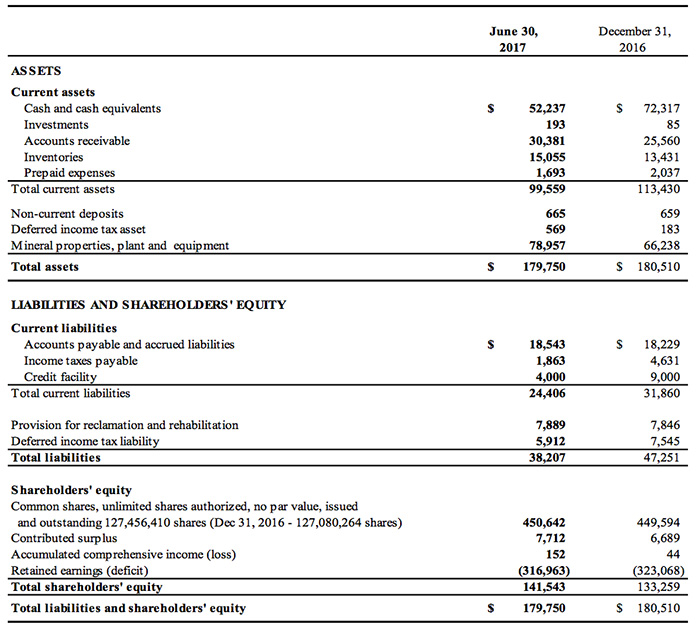

CONSOLIDATED INTERIM STATEMENTS OF FINANCIAL POSITION

(expressed in thousands of US dollars)

This statement should be read in conjunction with the condensed consolidated interim financial statements for the period ended June 30, 2017 and the related notes contained therein.